輸入取引を行っていればいつかは税関事後調査の対象となります。

そこで何かしらの関税の計算に関わる不備があれば過去5年まで遡って

追徴課税が課され、企業、個人問わず大きな金銭的損害を受ける事になります。

税関事後調査は全国の輸入者を満遍なく回るという形ではなく、限りある時間の中で

追徴課税が大きいと予想される特定の輸入者に狙いを定めて実施されます。

そのため税関は事後調査先を決定する前に入念に輸入者を下調べする事になり、日々

輸入通関を行う貨物の実物から得られる情報や輸入者のホームページ等から取扱い品目

の詳細、価格、仕様、更には取引先企業、関連企業等あらゆる情報を収集しています。

しかし、いかに税関といえども全ての輸入者の情報を把握する事は困難です。

例えば貨物や通関書類に特別注目すべき情報が無く、輸入者のホームページも無いとい

う場合、税関は輸入者に対し「どのような輸入者なのか」と事業形態等の会社情報を報

告させる事があります。

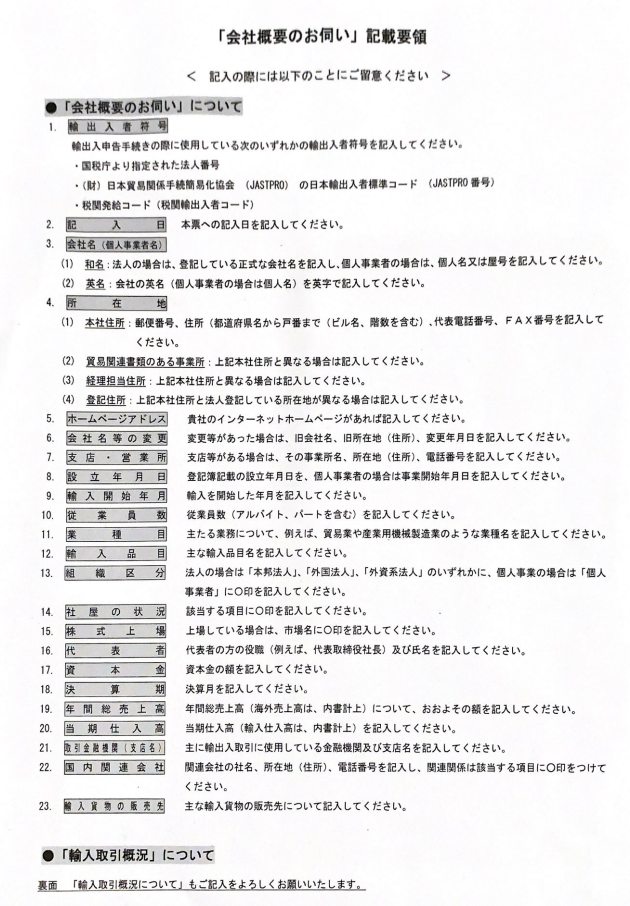

これは「会社概況調査のご案内」という手紙を輸入者に送付する事により行われます。

他にも「会社概要のお伺い」「会社概要の照会について」といったように税関各署に

よって呼び名は変わりますが、これが送付されたという事は税関側が輸入者の情報を

十分に把握できていないという事になります。

以下に会社概況調査書面の例を紹介します。

まずは会社の概要そのものについて具体的な質問がなされます。

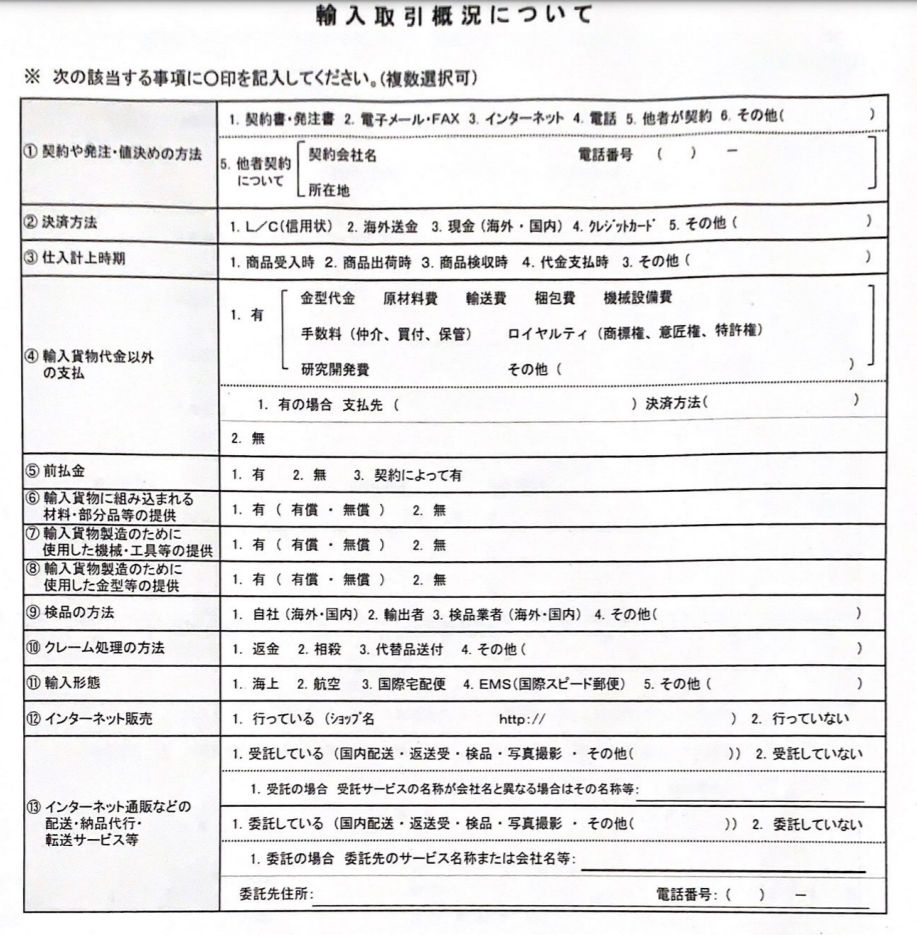

次に輸入取引概況についての質問になります。

輸入取引概況は事後調査を実施するかどうかの判断に大きく影響を与えます。

こちらを適当に記入してしまうと日々の輸入通関情報との矛盾、差異等が出てしまい、

税関の調査担当に不要な疑義を与えてしまう事により事後調査対象にされてしまう可能

性があります。

その為、この輸入取引概況は慎重に検討して記入する必要があります。

以下企業向けと個人、小規模輸入者向けに記載の際の注意点を解説します。

企業向け輸入取引概況記載時の注意点

ここでいう「企業」とは輸入品の企画、設計、デザイン等の製品開発に関わり、

国外の工場に製造を委託(OEM等)をして完成した製品を輸入する企業等を指します。

④~⑩は主に企業向けの質問で関税評価上の申告価格が適切かどうかを判断する為の

質問です。本記事の関税評価についてにおいて事後調査では関税評価漏れが指摘される

事により多額の追徴課税の対象になると解説しました。

以下に各項目に対して税関がどのように関税評価漏れから追徴課税を行うのかを

ざっくりと解説していきます。

④輸入貨物代金以外の支払い

インボイスに記載してある価格だけが申告価格ではなく、金型代金、原材料費、輸送費

、梱包費、機械設備費、手数料(仲介、買い付け、保管)ロイヤルティ(商標権、意匠

権、特許権)、研究開発費など様々な名目での支払いが輸入貨物代金以外に発生してい

る事があります。

上記のような貨物代金以外の支払いがあれば評価申告という形で輸入申告の課税価格に

含める必要がある場合があり、これが抜けていると評価漏れとなります。

事例:輸入者が支払った価格調整金の申告漏れ輸入者Dは、ドイツの輸出者から自動車等を輸入していました。Dは、輸出者との取決めに基づき、過去輸入した貨物について遡及して価格を見直し、増額となった金額を価格調整金として支払っていました。本来、この価格調整金は課税価格に含められるべきものでしたが、Dは修正申告を行っていませんでした。その結果、申告漏れ課税価格は103億7,105万円、追徴税額は8億3,166万円でした。出典:財務省HP

⑤前払い金

輸入貨物代金の支払いを複数回に分ける場合、支払った総額が課税価格になりますが、

例えば前払い金を支払った後の残金だけがインボイスに記載され、当該残額のみを申

告している場合、前払い金の額だけ申告漏れとなります。

事例:決済金額と異なる価格のインボイスを用いた申告漏れ輸入者Fは、中国の輸出者から鞄を輸入していました。Fの経理担当者はフランスの売手から送付された決済用インボイスに基づき貨物代金を支払っていましたが、Fの輸入担当者は輸出者が作成した決済金額と異なる価格が記載されたインボイスを用いて申告していました。本来、決済用インボイスの価格で申告するものでしたが、経理担当者と輸入担当者との連絡不足によりFは誤ったインボイスの価格で申告していました。その結果、その他の申告漏れも含め、申告漏れ課税価格は7億1,992万円、追徴税額は1億2,497万円でした。出典:財務省HP

⑥輸入貨物に組み込まれる材料・部分品等の提供

輸入貨物に組み込まれる材料・部品をあらかじめ無償で輸出者側に提供しているパター

ンでは無償で輸出した材料・部品の費用は当該完成品を輸入する際に評価申告を行う必

要があり、これが抜けていると評価漏れとなります。

事例:輸入者が無償提供した材料等費用の申告漏れ輸入者Eは、台湾の輸出者から医療用品を輸入していました。Eは、輸出者に対して輸入貨物の生産に必要な材料及び輸入貨物の製造に使用する設備を本邦所在のエンドユーザーから無償で提供させていました。本来、この材料等の無償提供に要した費用は課税価格に含めるべきものでしたが、Eは課税価格に含めずに申告していました。その結果、その他の申告漏れも含め、申告漏れの課税価格は23億2,596万円、追徴税額は1億8,869万円でした。出典:財務省HP

⑦輸入貨物製造のために使用した機械・工具等の提供

輸入貨物製造のために使用した機械・工具等をあらかじめ無償で輸出者側に提供してい

るパターンでは当該費用を当該完成品を輸入する際に評価申告を行う必要があり、これ

が抜けていると評価漏れとなります。

事例:輸入貨物に係る組立費用の申告漏れ輸入者Eは、韓国の輸出者から化粧品容器を輸入していました。Eは、輸出者に対して輸入貨物の組立費用をインボイス価格とは別に支払っていました。本来、この費用は課税価格に含めるべきものでしたが、Eは課税価格に含めずに申告していました。その結果、その他の申告漏れも含め、申告漏れ課税価格は14億2,123万円、追徴税額は1億9,071万円でした。出典:財務省HP

⑧輸入貨物製造のために使用した金型等の提供

輸入貨物製造のための金型等をあらかじめ無償で輸出者側に提供しているパターンでは

当該費用を当該完成品を輸入する際に評価申告を行う必要があり、これが抜けていると

評価漏れとなります。出典:財務省HP

事例:輸入者が提供した部材の金型費用の申告漏れ

輸入者Cは、ベトナムの輸出者から自動車部品を輸入していました。Cは、自動車部品に組み込まれる部材を輸出者に有償で提供していましたが、部材の金型費用については輸出者への有償提供価格に含めていませんでした。本来、この金型費用は課税価格に含めるべきものでしたが、Cは課税価格に含めずに申告していました。その結果、その他の申告漏れも含め、申告漏れ課税価格は5億4,211万円、追徴税額は5,825万円でした。出典:財務省HP

⑨検品の方法

輸入貨物の検品や検査などが必要な場合、ケースバイケースですが評価申告を要する場

合があります。

例えば輸入者の都合で検品や検査を行い、費用が発生する場合は評価申告が不要になる

事がありますが、輸出者側の都合での検品や検査が必要な場合で輸入者がその費用を負

担する場合は当該費用を評価申告する必要がある場合があります。

⑩クレーム処理の方法

輸入貨物に問題があった場合、輸出者に対しクレームを入れる事になりますが、その

解決方法によって評価申告が必要になる場合があります。

例えばある貨物を$10,000で輸入し、不良品である事を理由に輸出者にクレームを入れ

たとします。その際に輸出者が次回の同量の輸入品は前回輸入分の不良品の数量分であ

る$2,000を引いて$8,000で購入できるという提案をした場合、次回輸入時のインボイ

ス価格も支払う額も$8,000ではありますが、関税評価のルールではこのような状況に

あったとしても2回目の輸入は$10,000で申告をしなければいけないとなっています。

クレーム相殺によって実際の支払い価格から$2000割り引かれていても申告時は割引前

の価格で申告しなければ評価漏れとなります。

以上が企業向け評価申告漏れの有無を確認する為の輸入取引概況報告となります。

これを見ると全て「無」を選択すれば問題ないと考える方もいるかと思いますが、

日々の輸入申告での貨物検査、書類審査において実際の通関状況と概況報告とで

矛盾が発見された場合は税関からの印象が非常に悪くなりますので概況報告は正確に

記載する必要があります。

以上輸入取引概況への記載は税関に追徴課税の機会を与える可能性がありますので

慎重に記載を行ってください。

もしご自身で評価申告漏れがあることが確認できましたらできるだけ早めに評価の

事前教示を受ける事と修正申告を行う事をお勧めします。

個人、小規模輸入者向け輸入取引概況記載時の注意点

ここでいう「個人、小規模の輸入者」とは例えばebay,タオバオ,アリババ等の海外通販

から仕入れを行い、国内でアマゾン、ヤフオク、メルカリ等へ出品したり、HPを利用

して日本国内で販売する事業形態の事を指します。

「個人、小規模の輸入者」が輸入取引概況に記載する場合、⑫~⑬は慎重に検討し、

記載する必要があると考えます。

⑫インターネット販売

税関は輸入者のホームページを確認し、情報を収集しています。その為、輸入者が

どのようにネット販売をしているかを把握できていない場合は本項目から報告させ

る事により、以後当該ホームページを訪問し、製品の特長、機能、価格等の情報を

収集し、アンダーバリューの疑いが無いかどうかを確認する事になります。

⑬インターネット通販などの配送・納品代行・転送サービス等

本項目は少々複雑で、国内での輸入貨物の流れによって課税価格が変わる場合に輸入者

が適切な価格で申告ができているのかを確認しています。

例えば国内に住所を有しない者(輸出者等)が国内の販売代行業者等に貨物を直接送付

し、日本国内で販売している事業形態である場合、インボイス価格が申告価格にならな

い場合があります。(海外居住者がアマゾンFBA等に委託して国内販売をする場合等)

また、貨物の転送業者によっては悪質なアンダーバリューを繰り返している者がいます

ので、このような転送業者を使用している輸入者は税関からマークされる可能性があり

ます。

事例:非居住者からの委託で輸入される貨物の申告誤り輸入者Dは、中国の輸出者から家具等を輸入していました。Dは、非居住者が本邦のEC(電子商取引)サイトで販売する予定の家具等の通関手続及び国内運送を輸出者から請け負っていましたが、適正な方法で課税価格を計算せず、輸出者が作成したインボイスに基づき申告していました。

その結果、その他の申告漏れも含め、申告漏れ課税価格は2億4,101万円、追徴税額は2,201万円でした。出典:財務省HP

以上輸入取引概況への記載は税関に追徴課税の機会を与える可能性がありますので

慎重に記載を行ってください。